The SSP rules changed on 6 April 2026. If you haven’t updated your payroll yet, you may be underpaying staff right now.

The Employment Rights Act 2025 rewrote the rules. No more waiting days. No more earnings threshold. These aren’t minor updates. They’re the biggest SSP changes since the 1980s.

This guide is for employers, payroll managers, HR teams, company directors, and employees. By the end, you’ll know exactly what SSP you owe or are owed in 2026.

Statutory Sick Pay Overview for 2026

What Is the Current SSP Rate?

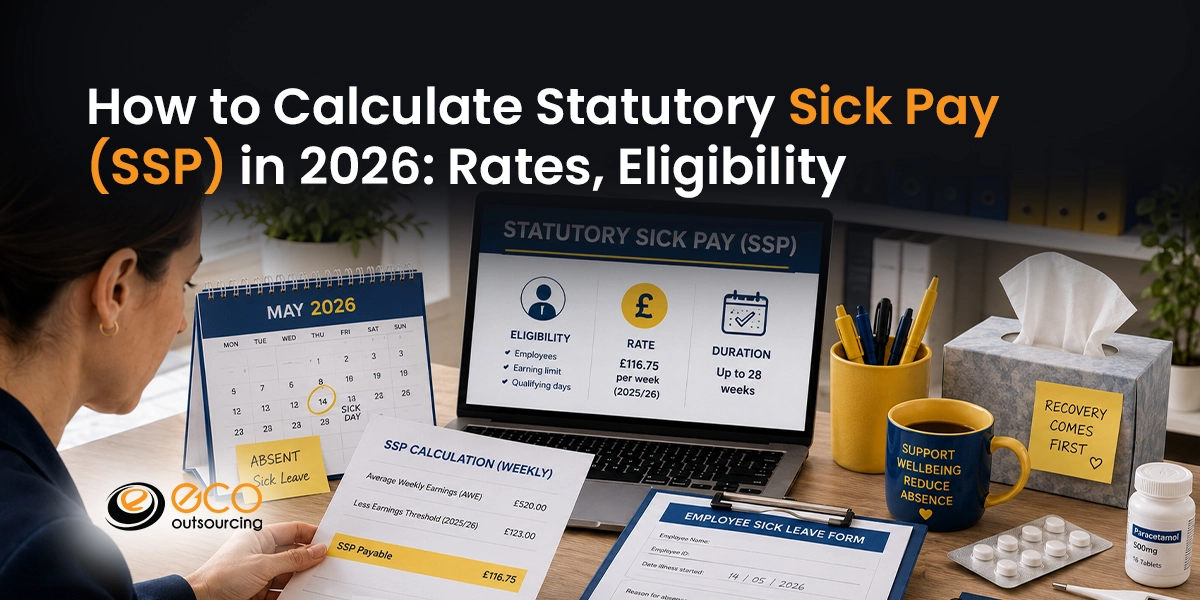

The statutory sick pay weekly rate for 2026/27 is £123.25 per week. That’s £24.65 per day for a five-day-week worker.

Lower earners don’t get the flat rate. From 6 April 2026, SSP is the lower of 80% of average weekly earnings or £123.25. We’ll show you how this works with real examples.

Key SSP Facts for 2026

| Detail | 2026/27 Rule |

|---|---|

| Weekly SSP Rate | £123.25 |

| Daily SSP Rate (5 Qualifying Days) | £24.65 |

| Waiting Days | None. SSP is paid from day one. |

| Earnings Threshold | Removed. All employees qualify. |

| Maximum Entitlement | 28 weeks. |

| SSP Taxable? | Yes. Income Tax and National Insurance apply. |

| Calculation Method | Lower of 80% of Average Weekly Earnings (AWE) or £123.25. |

| Enforcement Body | Fair Work Agency (from 7 April 2026). |

What Changed in Statutory Sick Pay in 2026?

Statutory sick pay changes from 6 April 2026 cover three key areas:

- SSP is paid from day one. The three waiting days no longer exist.

- The Lower Earnings Limit of £125 per week has been removed.

- Lower earners now get 80% of their average weekly earnings.

These changes are permanent. Every UK employer must apply them now.

What Is Statutory Sick Pay and How Does It Work?

Understanding SSP

Statutory Sick Pay is the legal minimum your employer must pay when you’re off sick. It doesn’t come from HMRC. Your employer pays it directly.

Before April 2026, you needed to earn at least £125 per week to qualify. That rule is gone. Many more workers now have SSP rights.

SSP vs Company Sick Pay

SSP is the minimum. Some employers pay more through Contractual Sick Pay. This should appear in your employment contract.

If your employer only offers SSP, you’ll get £123.25 per week or 80% of your average weekly earnings, whichever is lower.

Who Pays Statutory Sick Pay?

Your employer pays SSP through payroll. They can’t reclaim it from HMRC under standard rules. It’s a direct employer cost.

in 2026: Rates, Eligibility")

Statutory Sick Pay Changes in 2026

Overview of the Employment Rights Reforms

Changes to statutory sick pay under the Employment Rights Act 2025 took effect on 6 April 2026. The Act received Royal Assent on 18 December 2025.

Around 1.3 million more workers now qualify for SSP. Most of them are on low pay or zero-hours contracts.

SSP Rules Before and After April 2026

| Rule | Before April 2026 | From 6 April 2026 |

|---|---|---|

| Waiting Days | 3 unpaid days | None. Paid from day one |

| Earnings Threshold | £125/week minimum | No minimum. All qualify |

| SSP Calculation | Flat rate only (£116.75) | Lower of 80% AWE or £123.25 |

| Low Earners | Not eligible | Now eligible |

| Enforcement | No dedicated body | Fair Work Agency |

How the New Rules Affect Employees

If you earn less than £154.06 per week, you’ll get 80% of your average weekly earnings. That may be less than £123.25. But it’s better than nothing.

If you earn above £154.06 per week, 80% of your earnings exceeds £123.25. The flat rate applies as the cap.

How the New Rules Affect Employers

Every qualifying absence now costs money from day one. ACAS puts the total extra UK employer cost at roughly £450 million per year. That’s about £15 per employee annually.

The Fair Work Agency launched on 7 April 2026. It can fine employers 200% of any unpaid SSP, up to £20,000 per worker.

Common Misunderstandings About the 2026 Changes

- ‘My employee was already on SSP before April.’ They keep the flat rate under transitional protection for that continuous absence.

- ‘We’re a small business, so we’re exempt.’ There are no size exemptions. All UK employers must comply.

- ‘Day-one unfair dismissal rights also changed in April.’ This is wrong. That change takes effect in January 2027.

Who Is Eligible for Statutory Sick Pay?

Basic SSP Eligibility Requirements

From 6 April 2026, an employee qualifies for SSP if they meet all four conditions below.

- They’ve done some work under their contract

- They’re classed as employed for tax purposes and paid via PAYE

- They’re absent for at least one full qualifying day

- They told their employer within the agreed deadline or within 7 days

There’s no longer any earnings requirement. An employee earning £50 a week now qualifies. They’ll receive 80% of that amount.

Can Zero-Hours Contract Workers Claim SSP?

Statutory sick pay on a zero-hours contract now applies to all PAYE workers. The earnings threshold removal changed everything for this group. Many zero-hours workers previously earned below £125 per week and got nothing.

The tricky part is calculating their average weekly earnings.

Can Temporary and Seasonal Workers Claim SSP?

Yes. They need to be on PAYE, have done some work, and be off sick on a day they’d normally work. Agency workers also qualify if paid via PAYE through their agency.

Who Does Not Qualify for SSP?

- Self-employed individuals not on PAYE

- Employees who haven’t started work yet

- Workers who’ve already received 28 weeks of SSP

- Those off sick for a pregnancy-related reason in the 4 weeks before their due date

Can Self-Employed People Get Statutory Sick Pay?

Why Self-Employed Workers Cannot Claim SSP

Statutory sick pay self-employed is not available. SSP is an employment right. It only covers people paid through PAYE.

If you file taxes through Self-Assessment, SSP doesn’t apply to you. Self-employed and statutory sick pay simply don’t go together under UK law.

What Financial Support Is Available Instead?

You have three main options if you’re self-employed and too ill to work.

- New Style Employment and Support Allowance. This requires sufficient National Insurance contributions.

- Universal Credit. This depends on your household income and savings.

- Income Protection Insurance. This is useful if you have a private policy in place.

Check your NI record now, before you need to make a claim. ESA depends on your contribution history.

What If You Operate Through a Limited Company?

This is worth knowing. If you’re a director and you pay yourself a salary via PAYE, you may qualify for SSP.

With the Lower Earnings Limit removed, even a small PAYE salary can trigger SSP rights. See Example 6 below for a full director walkthrough.

How to Calculate Statutory Sick Pay Step by Step

Step 1: Confirm Employee Eligibility

Check the employee has done some work, is on PAYE, and is absent on a normal working day. If they didn’t tell you within 7 days, you can withhold SSP.

Step 2: Identify Qualifying Days

Qualifying days are the days the employee is contracted to work. A Monday-to-Friday employee has five qualifying days per week. Part-time workers may have fewer. This affects the daily rate.

Step 3: Calculate Average Weekly Earnings

Use the 8 weeks ending just before the first sick day. Add up all gross earnings across those 8 weeks. Divide by 8. That’s the AWE.

For new starters, use earnings from the weeks worked instead.

Step 4: Apply the SSP Rate

Work out 80% of the AWE. Compare it with £123.25. Pay whichever is lower.

Calculating statutory sick pay per day: divide the weekly rate by the number of qualifying days. For a 5-day worker: £123.25 divided by 5 equals £24.65 per day.

Step 5: Record SSP Correctly in Payroll

Process SSP through PAYE. Show it on the payslip. Deduct Income Tax and NI as normal. Keep records of all sick dates, AWE workings, and payments for at least 3 years.

in 2026: Rates, Eligibility")

Understanding the SSP Weekly Rate and Daily Rate

How the Weekly SSP Rate Is Applied

The statutory sick pay weekly rate of £123.25 covers a full week of qualifying sick days. It doesn’t apply to calendar days. It only covers days the employee would normally work.

Why Employees Sometimes Get Different SSP Amounts

Two things cause this. Their AWE may be below the level where the flat rate kicks in, so they get 80% of earnings instead. Or they have fewer qualifying days than a standard 5-day worker.

Statutory Sick Pay for Part-Time Employees

Do Part-Time Workers Receive Less SSP?

Not always. The weekly cap stays at £123.25. But the daily rate is higher for part-time staff because the same weekly cap spreads across fewer days.

A 3-day worker’s daily rate is £41.08. A 5-day worker’s daily rate is £24.65. The weekly maximum is the same for both.

How SSP Is Calculated for Part-Time Staff

The steps are the same as for full-time workers. Confirm eligibility. Find the qualifying days. Calculate AWE. Apply the lower of 80% or £123.25.

The only change is the divisor for the daily rate. Fewer qualifying days means a higher daily SSP amount.

Statutory Sick Pay on Zero-Hours Contracts

Do Zero-Hours Workers Qualify for SSP?

Yes. From 6 April 2026, all zero-hours workers on PAYE qualify for SSP. This is one of the most important changes in the new rules.

How Average Weekly Earnings Are Calculated

Use actual gross earnings paid in the 8 weeks before the illness. Include regular pay but not expense refunds.

If someone only worked 3 of those 8 weeks, you still divide total earnings by 8. Dividing by weeks actually worked is a common and costly mistake.

Common Zero-Hours Contract SSP Problems

- Dividing earnings by weeks worked instead of 8

- Using net pay instead of gross pay

- Leaving out commission or regular overtime

- Treating a PAYE worker as self-employed by mistake

Is Statutory Sick Pay Taxable?

Does SSP Count as Taxable Income?

Yes. HMRC treats SSP as employment income. Income Tax and National Insurance apply, just like normal pay.

National Insurance and Pension Contributions on SSP

Employee NI comes off SSP as normal. Employer NI is also due. Whether SSP counts toward pension auto-enrolment depends on your scheme rules. Check your pension contract for details.

Why Your SSP Payment May Be Lower Than Expected

Tax and NI reduce the gross amount. A basic-rate taxpayer receiving £123.25 gross will take home around £100 or less. This depends on their tax code and NI position.

Can You Receive SSP From More Than One Employer?

Working Multiple Jobs and SSP Entitlement

Yes. If you work for two employers and qualify with both, you can receive SSP from each one. Each employer checks your entitlement using only their own payroll records.

They don’t need to contact each other. Your combined SSP from two jobs can exceed the single flat rate.

Statutory Sick Pay in Scotland

Are SSP Rules Different in Scotland?

Statutory sick pay Scotland follows the same rules as the rest of Great Britain. SSP is a UK-wide right under Westminster law. The April 2026 changes apply to Scottish employers and employees equally.

The Fair Work Agency covers the whole of Great Britain. Any underpayment complaint can go through the same enforcement process as in England and Wales.

What Happens When Statutory Sick Pay Ends?

How Long Can SSP Be Paid?

SSP runs for a maximum of 28 weeks per period of incapacity. It stops at 28 weeks, even if the employee is still off sick.

What Happens After the 28-Week Limit?

Your employer must issue an SSP1 form. This confirms SSP has ended and lets the employee apply for New Style Employment and Support Allowance or Universal Credit.

Benefits and Support Available After SSP

- New Style ESA for those with sufficient NI contributions

- Universal Credit for those without enough NI qualifying years

- Personal Independence Payment for long-term health conditions

Common Statutory Sick Pay Mistakes Employers Make

Miscalculating Average Weekly Earnings

This is the most common error. Some teams use net pay instead of gross. Others divide by weeks worked rather than the full 8-week period. Both lead to underpayment. The Fair Work Agency treats underpayment as a breach.

Using Incorrect Qualifying Days

If you apply a 5-day schedule to a 3-day worker, the daily rate is wrong. Match qualifying days to the actual work pattern every time.

Applying Outdated SSP Rules

Still using the 3-day wait? Still checking for the £125 earnings limit? Both rules are gone. Using old rules after 6 April 2026 is a breach and can trigger a 200% underpayment penalty.

Errors With Zero-Hours and Variable-Hours Staff

Include all PAYE earnings in the 8-week reference period. Don’t skip weeks where the worker earned nothing. Those weeks still count in the divisor.

Missing Linked Periods of Sickness

Two sickness spells are linked if they’re 8 weeks or less apart. Linked spells count as one continuous absence for the 28-week SSP limit. Missing this can lead to overpaying SSP past the legal limit.

Failing to Keep Accurate Records

HMRC can ask for SSP records going back 3 years. If you can’t show how, you worked out the AWE, which days were qualifying days, and what you paid, you’re at risk. Record every absence, including single-day events.

SSP Compliance Checklist for Employers

Eligibility Checks

- Confirm the employee is on PAYE and has done some work

- Check that the absence falls on a qualifying day

- Confirm the employee gave notice within 7 days

- Check that the employee isn’t in an excluded group

Payroll Processing Checks

- Calculate AWE using 8 weeks of gross earnings

- Pay the lower of 80% AWE or £123.25

- Use the right number of qualifying days for the daily rate

- Deduct Income Tax and NI from the SSP amount

- Show SSP as a separate line on the payslip

Record-Keeping Requirements

- Keep all SSP records for at least 3 years

- Record sick dates, AWE calculations, and amounts paid

- Issue an SSP1 form when SSP ends or when the employee doesn’t qualify

HMRC Compliance Requirements

- Report SSP through RTI via Full Payment Submission

- Respond promptly to Fair Work Agency requests

- Update payroll software for the 2026 rule changes

FAQs: Business Process Outsourcing for SMEs

Yes. From 6 April 2026, zero-hours workers on PAYE qualify regardless of what they earn. AWE is based on the 8 weeks before the illness.

Statutory sick pay for self-employed people is not available. SSP is for PAYE employees only. Self-employed people can look at New Style ESA or Universal Credit instead.

Yes. SSP is subject to Income Tax and National Insurance in the same way as regular wages.

The weekly rate stays the same. The daily rate is higher because fewer qualifying days divide into the same weekly cap.

The 2026 reforms cover England, Scotland, and Wales. Northern Ireland has separate legislation. Employers there should check with the Department for Communities.

The 2026 reforms cover England, Scotland, and Wales. Northern Ireland has separate legislation. Employers there should check with the Department for Communities.

What Employers Should Do Now:

The SSP rules have changed, and mistakes now carry real financial risk. Employers should make sure every sick pay calculation is supported by clear, accurate records.

- Use accurate average weekly earnings calculations.

- Apply the correct qualifying day rules for each worker.

- Treat SSP correctly for tax and National Insurance.

- Keep complete records of sickness dates, calculations, and payments.

The Fair Work Agency now actively enforces these requirements, so payroll accuracy is no longer optional.

Get Specialist Payroll Support

Need help getting SSP right? Eco Outsourcing provides specialist payroll support for SMEs, directors, and growing UK businesses.

Our team handles accurate SSP calculations and full PAYE compliance, helping you reduce the risk of Fair Work Agency penalties.

Contact our team today to speak with a payroll specialist.